TRUMP TAKES ON THE BANKS: A RECKONING FOR ILLINOIS CONSUMERS

FROM RURAL CHURCHES TO CITY STOREFRONTS, A NEW FIGHT OVER WHO CONTROLS YOUR MONEY IS ERUPTING IN ILLINOIS.

THE ERASURE

They can lock your doors. They can silence your voice. They can shut down your business. But when they cut you off from your own money—it’s not just an inconvenience.

It’s an erasure.

That’s the warning echoing from the Oval Office to every Illinois main street as President Donald J. Trump launches what he calls the biggest economic rights battle in fifty years.

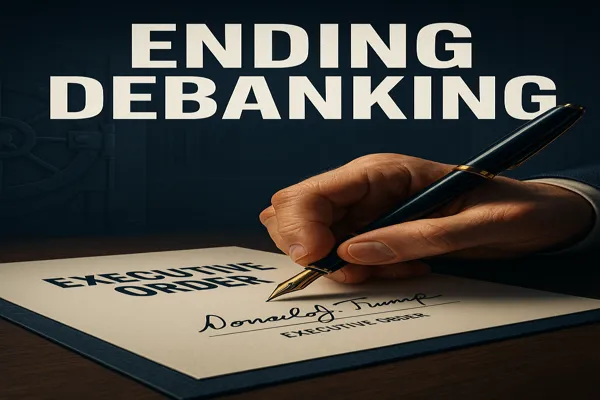

On a humid morning, August 7, 2025, Trump sat at the Resolute Desk, pen in hand.

Cameras flashed. Outside, protestors chanted while news helicopters circled overhead.

Inside, aides murmured about the lawsuits Wall Street lawyers were already drafting.

This wasn’t just another signing ceremony.

It was a challenge, thrown straight into the marble lobbies of America’s biggest banks.

The mission: End “debanking”—the quiet practice that, critics say, destroys livelihoods by cutting people off from ...

accounts,

credit,

and payment systems

simply for holding the “wrong” beliefs.

THE EXECUTIVE ORDER

Trump’s directive was blunt:

“No American should be denied access to financial services because of their constitutionally or statutorily protected beliefs, affiliations, or political views.”

The order tells federal regulators to erase the vague “reputational risk” standard, dig into past politically motivated account closures, and work with the Justice Department to hold banks accountable.

Supporters call it the modern-day equivalent of tearing down the walls of redlining—the discriminatory banking practice that once locked Black neighborhoods in Chicago out of loans under the excuse of “financial risk.”

Illinois historian Rebecca Lanning put it plainly:

“Redlining shut people out because of who they were. Debanking does the same—it’s just wearing a different mask.”

ILLINOIS: THE FIRST BATTLEFIELD

From Decatur’s grain silos to Springfield’s courthouse square, Illinois is now ground zero for this fight.

In Effingham, the morning sun was barely up when the credit card terminal at Hanley’s Gun & Tackle went dead.

Bill Hanley thought it was a glitch—until his bank called.

His merchant account was closed.

No fraud.

No bounced checks.

Just a cryptic “reputational risk” note.

“It was like they’d shut off the electricity,” Hanley said, standing beneath the deer mounts and faded flag in his store.

“No warning. No appeal. Just gone. I had customers in line.”

In Quincy, church treasurer Ellen Price tried to deposit Sunday’s offerings—only to find the account frozen.

In Carbondale, a food pantry’s debit card was declined in the grocery store checkout line.

One compliance officer admitted the truth:

“We’ve had clients flagged—not for fraud or money laundering—but because they were politically controversial or tied to crypto. This order gives us breathing room.”

THE PUSHBACK

Not everyone’s cheering.

The American Bankers Association warned the order could “compromise risk management,” forcing banks to take on clients they see as “operational or legal hazards.”

Progressive lawmakers in Illinois argue it could open the door for “predatory lenders and dangerous industries” to sneak into the system.

Supporters see it differently.

State Representative Adam Niemerg shot back:

“This isn’t about protecting Trump—it’s about protecting truck drivers, gun shop owners, and churches across Illinois who’ve been quietly dropped by banks just for what they believe.”

THE LEGAL SHOWDOWN

The ink was barely dry before the lawsuits began.

Banking groups are gearing up to challenge the order, arguing it exceeds presidential authority.

University of Illinois law professor Sara Winslow says the stakes are huge:

“This is about whether financial access is as essential to liberty as speech or religion. If the courts say yes, it could redefine the First Amendment.”

If it reaches the Supreme Court, the case could join the ranks of landmark decisions like Brown v. Board or Citizens United—reshaping the balance between corporate power and constitutional rights for generations.

THE BIGGER QUESTION

This fight is about more than regulations.

It’s about power—about who controls the lifeblood of the economy, and who gets cut off.

A former FDIC counsel didn’t mince words:

“If Americans can’t access their own money because someone in a boardroom didn’t like what they posted online—that’s a line we should never cross.”

Critics call it reckless.

Supporters call it protection from a kind of economic exile.

The image is stark:

A padlocked wallet.

A shuttered storefront.

A congregation unable to pay its bills.

Not because of crime. Not because of fraud. But because their beliefs were “too inconvenient.”

And that leads to the question every American must ask:

When the keys to your money belong to a few institutions, how long before they decide to lock the door?

THE ROAD AHEAD

The battle won’t just play out in Washington courtrooms—it’ll be felt in Illinois coffee shops, hardware stores, and churches.

Whether Trump’s order stands or falls, it has forced a national conversation:

Who controls your money—and should politics ever be a reason to take it away?

Because when the power to cut you off rests in the hands of a few, it’s not just your account that’s at risk.

It’s your freedom.

Cited Sources: Presidential Executive Order on Guaranteeing Fair Banking for All Americans, White House, August 7, 2025 Public remarks and interviews by Donald J. Trump, CNBC, August 2025 Illinois Department of Financial and Professional Regulation data, 2023 University of Chicago economic study, 2024 Interviews and statements from Illinois politicians, historians, economists, and banking officials